How to avoid health insurance headaches

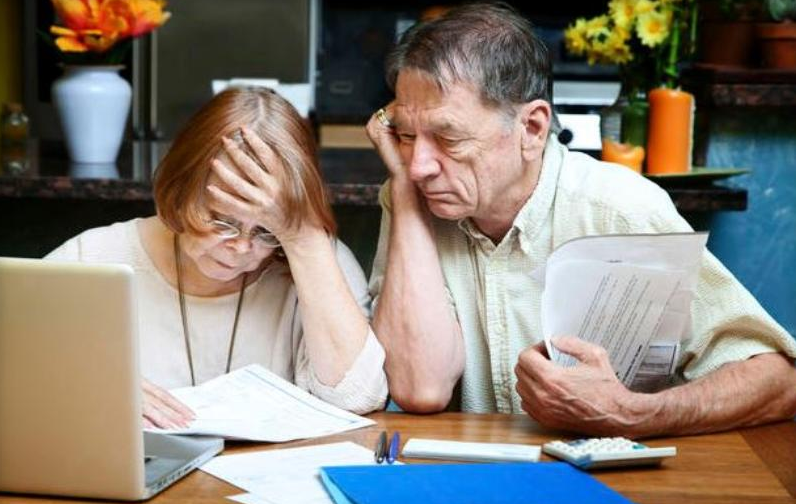

Do you find the topic of health insurance confusing?

Don’t stress. It’s okay if you do. In fact, you are far from the only one!

According to a recent article in the Sydney Morning Herald more than “44 percent of policyholders” blame complex policies for lacking the confidence to switch insurers despite feeling dissatisfied with their current provider.

These startling findings from a survey conducted by Choice have prompted the consumer group to call on the government to finally intervene and simplify health insurance policies to help all Australians take out the best coverage at the best price for them.

Choice’s analysis of nearly 1,000 respondents indicated that they were confused by “inconsistent terminology” and “technical language” – namely the use of industry jargon such as sub limits, gap bonuses and excess waivers. Terms often employed by sneaky providers to do exactly that: confuse you!

The survey also found that 21% of policyholders had planned to decrease or cancel their cover, attributing this decision to escalating costs.

So what measures can you implement to avoid further health insurance policy headaches and, ultimately, avoid forking out your hard earned for extras and benefits you don’t need?

You need to do a regular review to see if you still need all the cover you are paying for. Are you 65 and paying for pregnancy for example?

You can see every policy at the government website privatehealth.gov.au, or you can start with the special offer for FiftyUp Club members.

At the Club, we know our members find this product expensive and complex, and we are here to help you navigate your health coverage. In fact, thanks to our offer with HCF, switching has never been easier.

Take up HCF’s exclusive members only offer today and receive up to $400 cash back for families, couples, and single parent families who switch hospital & extras cover to HCF paid over 37 months of membership^. While singles could earn up to $200 cash back^.

Don’t prolong your headaches any longer; click here to find out more.

^If you take the special offer and remain with HCF, you may be eligible to receive up to $400. FiftyUp Club will pay by way of electronic funds transfer (EFT) $100 to eligible couples and families, after 3 months, 13 months, 25 months and 37 months. (Instalments for half these amounts will be made to singles). To be eligible to receive each instalment of cashback you must be a current member of HCF with hospital and extras cover at the point of expected instalment.

Cashback instalments will be paid by EFT only, to the bank account nominated by you; no cheques will be sent to members. To receive payment as a new or existing member, you must provide and must ensure that your nominated bank account details are provided correctly to FiftyUp Club. You should do so here.

Offer is for switchers only and excludes existing HCF customers. If you take up the offer and you are not already a member of the FiftyUp Club, you will become a member upon taking up the offer.

HCF will recognise waiting periods you've already served with your current fund. Some longer waiting periods and conditions apply. Any benefit limits used with your current fund will apply to your new HCF policy. Offer cannot be used in conjunction with any other corporate offer or discount.

FiftyUp Club receives a commission for each member who takes up an offer with HCF and remains a member of HCF. FiftyUp Club returns up to $400 of this commission to members in the form of the switcher's bonus/cashback, and shares the remainder with its media partners, which include Macquarie Media Ltd, Nova Entertainment and Nine Network Australia who provide the people power to make our campaigns successful. Part of our commissions will also be used to fund future FiftyUp Club Campaigns.